The Agentic Commerce Trap - Who Wins When AI Shops For You?

- Juanita Neville-Te Rito

- May 25

- 10 min read

Retailers are racing to become AI-ready with the best of intentions. They’re also, without realising it, building the infrastructure for their own race to the bottom – and funding the platforms that will run it.

I am genuinely pro-AI. I use it daily, I’ve said it in boardrooms, at conferences, heck I’ve even set up an AI business (rxcolab.ai for those of you unaware). The technology is incredible (at times scary), the productivity gains are real, and the retailers who treat it as a passing fad will pay for that complacency.

Which is exactly why what I have written matters. This isn’t a sceptic’s argument. It’s a thoughtful strategist’s point of view...... and the argument is uncomfortable, because the retailers making the decisions I’m about to describe aren’t being reckless. They’re being diligent. They’re doing what every expert, platform partner, and industry conference is telling them to do. And that’s precisely the problem.

THE SETUP

Agentic commerce – where AI agents act on behalf of consumers to discover, compare, and purchase products autonomously – is already transactional. According to Adobe's Cyber Week data, e-commerce traffic from generative AI platforms grew 693% in November and December 2025 compared to the same period the year before. In ANZ, 77% of retailers say AI agents will be essential for them to compete within a year, and 74% are increasing AI spending accordingly (Salesforce Connected Shoppers Report, 2025).

On the consumer side, 6 in 10 Australian shoppers are now comfortable using AI for shopping, with 32% already using it for shopping advice (Australia Post eCommerce Report, 2026). And 30% of consumers surveyed in late 2025 said they were willing to let an AI agent complete purchases on their behalf. That number is moving in one direction only.

The retailer response has been entirely rational: clean the product data, structure the catalogue, optimise for AI discovery. Be findable. This is GEO, (Generative Engine Optimisation), and it’s the latest must-have in the industry's playbook, with enterprise retainers now running $10,000 to $25,000+ a month.

Every one of these decisions makes sense in isolation. Together, they form a trap.

Retailers aren’t being reckless. They’re being diligent. They’re doing exactly what every expert and platform partner is telling them to do. That’s precisely the problem.

WHAT RETAILERS ARE ACTUALLY BUILDING

When an AI agent acts on behalf of a consumer, it doesn’t browse. It doesn’t respond to store atmosphere, brand warmth, or the carefully curated Instagram grid. It queries APIs, evaluates price and availability in real time, and completes transactions end-to-end. The consumer isn’t present at the moment of purchase. Their agent is.

Retail has always competed on multiple dimensions: price, yes, but also experience, trust, identity, and emotion. The brands that have built the strongest businesses in retail have done it through genuine differentiation – a distinct point of view, brand equity that means something beyond the ticket price, customer experiences that can’t be easily replicated. That differentiation is what shifts a purchase decision away from a pure price calculation. The consumer agent collapses it. It reduces a complex, human decision to a data query. In a data query, the lowest number wins.

Loyalty programmes are a precise example of how this plays out. They have always relied, partly, on customer friction – the forgotten points balance, the unredeemed offer, the lapsed reward. In the industry this is called breakage, and it is a material contributor to programme economics. Retailers have, largely without intending to, built loyalty programmes that work partly because customers don’t fully use them. AI agents eliminate this entirely. They don’t forget. They don’t miss the activation window. At scale, that’s not a theoretical risk – it’s a direct transfer of value away from the retailer, and almost no one has modelled it.

McKinsey illustrates the end-state: agents operating against standing goals rather than one-off transactions..... ‘Keep household essentials under $300 per month.’ With the shopper becoming episodic, stepping in only for meaningful decisions while the agent handles everything else - including, it will note, that your competitor has the same product for $1.20 less.

By making product data clean, structured, and perfectly machine-readable – which is exactly what GEO requires – retailers are removing the friction that previously slowed that comparison down. Different websites, different formats, different navigation: that friction wasn’t just inconvenient for customers. It was working in retailers’ favour. It created moments where something other than price could influence the outcome.

To be precise: GEO itself isn’t the problem, and being discoverable matters. The problem is doing it without understanding what you’re optimising for, and for whom. If the answer is ‘for consumer agents to find my lowest price faster,’ you’re not building competitive advantage. You’re accelerating your own commoditisation.

THE CONVERSION RATE TEMPTATION – AND WHAT THE REAL WORLD IS SHOWING

Here is where the trap gets more sophisticated......because there is a genuinely compelling number on the other side of this argument, and it deserves honest scrutiny.

ChatGPT’s Instant Checkout launched in late 2025 with reported conversion rates nearly nine times higher than Google organic search. For a retailer making the channel decision, that differential was hard to ignore and it is the reason smart, rational people opted in.

The reality has since proved more complicated. By March 2026, OpenAI had quietly scaled back Instant Checkout, routing purchases back to retailer websites rather than completing them inside ChatGPT. The conversion premium may be real for AI-assisted discovery. Whether it survives the full transaction journey remains unproven and the platforms are still working it out.

This matters because it illustrates something ANZ retailers should be watching carefully: the model is being tested, adjusted, and revised in real time in the US market, with merchants absorbing the friction of each iteration. ANZ retailers are making infrastructure and optimisation decisions right now based on a product that is still finding its shape. That is not a reason to disengage. It is a reason to engage with eyes open rather than in a sprint to keep up.

The fee structure is already visible in the US:

From January 2026, US Shopify merchants pay OpenAI a 4% transaction fee on purchases completed through ChatGPT’s checkout – confirmed by Shopify and reported by PYMNTS and Retail Brew – on top of existing subscription and processing costs.

For a $100 order, combined platform and processing fees run to approximately $7.20 before a cent has been spent on product, staff, rent, or freight.

ChatGPT Instant Checkout is not yet widely available to ANZ merchants, but the payment infrastructure is already arriving: Mastercard’s Agent Pay went live with Commonwealth Bank in Australia in January 2026 and Westpac NZ in February 2026.

ANZ retailers are making GEO and agentic readiness investments right now without knowing the fee structure they’re building toward. The US market is showing them exactly what it looks like.

THE ANZ CONTEXT THAT CHANGES THE MATHS

That fee structure deserves particular scrutiny in ANZ, where the economics of online retail are already difficult and the role of physical retail is fundamentally different to the markets where agentic commerce is being built.

In Australia, 76% of retail spend still happens in physical stores (Australia Post eCommerce Report, 2026).

In New Zealand, the figure is closer to 90% (NZ Post Annual eCommerce Review).

These are not lagging markets waiting to catch up with a more digital future – they are markets where physical retail genuinely dominates because geography, population density, and consumer behaviour make it so.

The cost to serve an online-only transaction – fulfilment, returns, last-mile delivery across dispersed populations, and now platform fees – is structurally higher than in-store.

Most ANZ retailers have quietly absorbed that cost imbalance for years in exchange for channel growth. Layering agentic commerce fees on top of an already cost-heavy channel compounds a problem that hasn’t been solved.

More fundamentally, this is an argument about who the customer actually is. The most sophisticated retailers have spent years understanding that their customer isn’t an ‘online shopper’ or a ‘store shopper’ – they are the same person, moving fluidly between channels depending on the day, the category, and the moment.

Research from ShipStation and Retail Economics found that $15 billion – nearly half of Australian online non-food sales in 2023 – involved a physical touchpoint at some stage of the journey. The omnichannel customer isn’t a choice between online and physical. They are both, and more.

A commerce strategy that optimises purely for the AI-mediated digital transaction, at the expense of the relationship that physical retail builds and sustains, is solving for the wrong version of the customer.

An agentic agent that completes a transaction efficiently tells you nothing about why that customer came back, what made them choose you over the competitor at $1.20 less, or what experience created the preference the agent is now executing. That context – the human, relational, experiential layer of retail – is where ANZ retail has historically been strong. It is also exactly what agentic commerce, by design, renders invisible.

ANZ retailers are making permanent infrastructure decisions based on a model that’s still being tested, adjusted, and revised in real time. The US market is the trial. ANZ retailers are watching it and calling it a roadmap.

FOLLOW THE MONEY

The Board Director who told me recently that ‘AI can do all this stuff for free’ is not alone. It’s a view I’m hearing across the industry. It is the single most expensive misconception in retail strategy right now.

OpenAI is projected to lose $14 billion in 2026 – not despite having 900 million weekly ChatGPT users, partly because of them. Deutsche Bank analysts have noted that no startup in history has operated with losses at this scale. OpenAI spends approximately $1.69 for every dollar of revenue it generates, and does not project profitability until 2029 at the earliest.

These platforms are burning investor capital to acquire users and market position. That capital will be recovered. The 4% on ChatGPT checkout is the opening position, not the ceiling. And as the Instant Checkout retreat shows, even that opening position is still being negotiated – with merchants and consumers as the test subjects.

At the infrastructure layer, Google’s Universal Commerce Protocol – built with Shopify integration and endorsed by Amazon, Meta, Microsoft, Salesforce, and Stripe – is positioning Google as foundational commerce infrastructure. The standard is described as open. So was the internet. The pattern is identical to every prior platform wave:

– Google and SEO: optimise for us, we’ll send you traffic – until AI Overviews answered the query and kept the traffic inside Google’s own ecosystem.

– Social commerce: build your audience on our platform – until reach became pay-to-play.

– Marketplaces: list with us for visibility – until the margin was gone and the retailer became a fulfilment arm.

Retailers are committing to the agentic commerce layer before the fee structure is fully visible, before the protocol wars are settled, and before the platforms’ profitability imperative has fully arrived. Each individual decision is defensible. The cumulative direction is not.

WHO’S LEANING IN – AND WHAT IT ACTUALLY SIGNALS

The large end of ANZ retail has moved decisively and, at their scale, it makes strategic sense. Woolworths committed to $400 million in AI-driven cost savings and became the first Australian retailer to adopt Google’s agentic platform, evolving its Olive chatbot into what it describes as an ‘intuitive partner’ that anticipates customer needs.

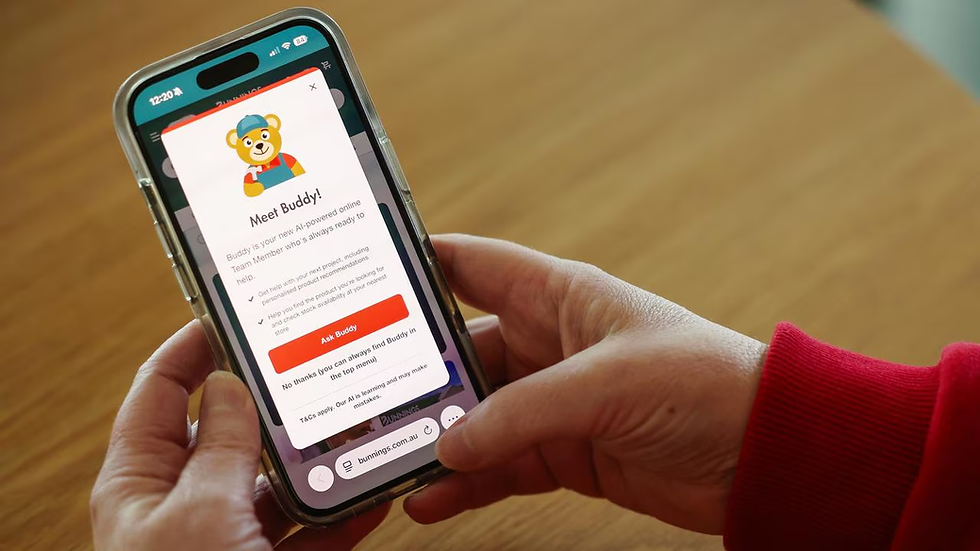

Bunnings; whose own leadership has acknowledged its technology capability has been widely underestimated, has launched Buddy, an AI-powered agentic assistant built on Google Cloud’s Gemini platform, describing agentic commerce as a ‘big bet’ for the business.

Both are building their own agentic layer, which is the right instinct: retailers without their own agentic infrastructure risk being reduced from brand destinations to inventory suppliers for someone else’s platform. But Woolworths and Bunnings have the data infrastructure, loyalty scale, and balance sheets to make this bet on their own terms. Their commitment is not a green light for every retailer. It is a signal that the large end of the market is staking out territory while the rules of engagement are still being written.

For SME retailers, the right investments right now are the ones that serve you in any channel regardless of which protocol wins: clean product data, accurate inventory, and a direct customer relationship that no platform can mediate away. The practical window to understand this landscape before being forced into it is probably 12 to 18 months. Use it.

THE REGULATORY COLLISION NOBODY IS TALKING ABOUT

Dynamic pricing and agentic commerce are heading directly into a regulatory environment that is tightening fast, and the grocery sector is the clearest signal of what’s coming for retail broadly.

In Australia, new regulations taking effect 1 July 2026 prohibit large retailers from charging excessive prices, with penalties of up to $10 million, three times the value of the benefit derived, or 10% of company turnover (ACCC, December 2025). The ACCC has named retail pricing as a priority enforcement area for 2025-26. Across the Tasman, the Commerce Commission has filed criminal charges against Woolworths New Zealand and two North Island Pak’nSave stores for alleged misleading pricing and inaccurate promotional claims.

The collision point: in both Australia and New Zealand, establishing a genuine ‘was’ price before promoting a discount is a legal requirement. Price establishment; holding a price for a defined period before marking it as a special, exists to prevent consumers being misled about the value of a promotion. AI-driven dynamic pricing systems that continuously adjust prices create a direct conflict with this framework. An AI agent that finds and activates a ‘discount’ manufactured through algorithmic price movement is not a win. It’s a regulatory event waiting to happen.

Pricing systems that cannot produce clear, auditable pricing histories will not survive scrutiny in this environment. The reputational cost of a misstep in a market already primed for supermarket pricing scrutiny will far exceed any gain the algorithm delivered.

Each individual decision is defensible. The cumulative direction is not. And the platforms know exactly where it leads.

THE QUESTION RETAILERS NEED TO ANSWER

The retailers building toward agentic commerce readiness right now are not making bad decisions. They are making individually rational decisions inside a system that is designed – by others, for others’ benefit – to aggregate those decisions into an outcome that serves the platforms far more than it serves retail.

The unknowing part is the important part. Victims get sympathy. The unknowingly complicit get disrupted.

I read this and wrote it down to use at some point - jealous I didn't write it myself. "Nobody has figured it out, but everyone has FOMO," says Emily Pfeiffer, principal analyst at Forrester. "Everyone is prematurely rushing to market."

So the question for every retail leader, every senior leadership team and every board isn’t whether to engage with agentic commerce.

It’s whether you understand whose game you’re playing, whose infrastructure you’re building, and who picks up the bill when the platforms decide it’s time to be profitable.

When someone tells you AI is free, ask them who is paying for OpenAI’s $14 billion in projected losses this year.

The answer, in time, is you.

#RetailVoice2026 #Xfiles #NZRetail #ANZRetail #RetailStrategy #RetailLeadership #TheReckoningContinues #AgenticCommerce #AgenticAI #GEO #RetailMedia #FutureOfRetail

My cousin from Hamilton has been on a rant for weeks about how all online pokies are basically the same — just reskinned versions of the same old games with nothing new to offer. I figured I'd actually put his theory to the test, so after a bit of digging around online, I came across trending casino games new zealand levelup and honestly, the variety caught me off guard. There were games I hadn't seen anywhere else, with fresh mechanics and themes that actually felt like someone had put some thought into them. I ended up playing a few rounds and found a couple that I've been coming back to regularly, each with its own pace and style that kept…

https://keonhacai.cam/ mình ghé thử đúng kiểu lướt cho biết thôi, thấy mọi người nhắc nên tò mò xem giao diện ra sao. Vào cái là mình để ý ngay cách họ chia nội dung theo từng khối nhìn khá “sạch”, không bị nhồi chữ dày đặc nên mắt đỡ mệt. Kéo xuống vài đoạn là hiểu trang đang sắp xếp thông tin theo hướng nào, kiểu ai hay xem nhanh cũng bắt nhịp được. Mình cũng thích mấy bảng họ trình bày theo cột, nhìn lướt vẫn theo kịp chứ không bị rối như nhiều chỗ khác. Với lại cái menu để khá dễ thấy nên chuyển qua lại không phải tìm lâu, đúng kiểu tiện tay. Nói chung phần…